You structured the deal carefully. Majority stake. Board control. Veto rights. Financial oversight. Six months later, you cannot get a capital call met, financial reports arrive three weeks late, and every operational decision requires a conversation you are not invited to.

Joint ventures are rarely tested when markets are stable and parties remain aligned. The real pressure comes later, when funding tightens, timelines slip, regulations change or commercial priorities diverge. When that pressure arrives, ventures rarely fail through a single defining dispute. They erode more gradually — through delayed funding, restricted access to information, stalled approvals, shifting control or strategic paralysis — often long before any formal proceedings begin.

That dynamic is particularly acute in renewable energy and infrastructure projects, where the joint venture is often the project itself. It holds the licence, owns the key assets and sits directly in the regulatory firing line. Capital is deployed early into long-life assets that are expensive, and sometimes impossible, to redeploy elsewhere.

This Friction Point series examines the structural fault lines that determine who really controls the joint venture, how leverage shifts under strain and whether value is preserved when conditions turn.

The Control Paradox

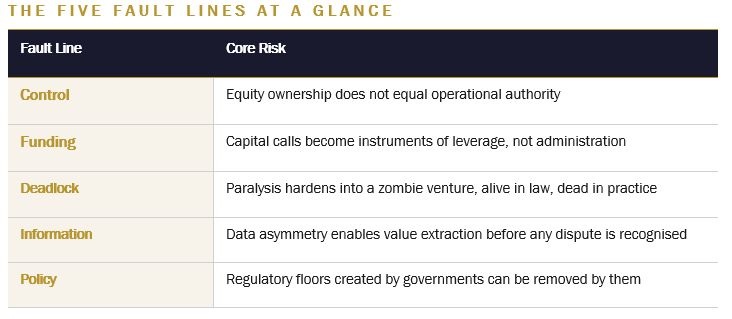

In some joint ventures, equity ownership does not necessarily translate into operational control. The investor in the opening scenario holds a majority stake. Yet real authority sits with the local partner that controls licenses, management access and regulatory relationships.

Board seats and veto rights may create the illusion of balance without delivering meaningful influence in practice. Stronger structures build control through management appointments, commitee design, procurement authority and financial reporting, not just the governance chart.

Funding Under Fire

Most joint venture agreements assume capital calls will be met in good faith. Under stress, however, the party able to delay or withhold funding often gains immediate leverage. In the scenario above, delayed contributions stall progress while shifting bargaining power at precisely the moment the project is most exposed.

Funding obligations stop functioning as administrative mechanics and become instruments of commercial pressure. Soft-default remedies such as interest penalties are often inadequate where non-payment is strategic.

For capital-intensive projects, particularly in renewables and infrastructure, agreements should be drafted on the assumption that a party may choose not to fund. Effective structures typically include automatic dilution mechanisms, suspension of non-essential rights and remedies aligned with external financing timelines.

Funding pressure is also rarely isolated. Delayed capital calls are almost always the first domino — they fuel delay, erode relationships and create the conditions in which the next fault line activates.

The Deadlock Trap

Deadlock is a predictable feature of long-term projects exposed to shifting markets, strained relationships and diverging commercial priorities. In the scenario above, stalled operational decisions are an early symptom. What begins as delay can harden into full paralysis.

Many deadlock clauses still assume parties will remain rational, aligned and financially stable throughout the life of the venture. When that assumption fails, escalation ladders, buy-sell provisions and valuation processes can become sources of paralysis, leaving projects frozen for months or years.

More resilient structures distinguish between operational and strategic deadlock, impose strict timelines and create exit routes that function without ongoing cooperation. In regulated sectors such as renewable energy, those mechanisms must also account for licensing requirements, lender consents and project contract restrictions.

The Information Advantage

The party that controls the management accounts controls the narrative — and the narrative determines whether there is a dispute at all. In stressed joint ventures, information quickly becomes leverage. In the opening scenario, financial information arrives late and incomplete, and by the time concerns crystallise, the commercial position may already have shifted.

The party controlling reporting systems, bank accounts, procurement channels or operational data can shape outcomes before legal remedies becomes available. Selective reporting, related-party transactions and inflated change orders can quietly erode value while remaining difficult to detect in real time.

Effective structures hard-wire transparency into the venture through direct bank visibility, dual signatory controls, restrictions on related-party transactions and independent technical or financial oversight. These systems must be negotiated at the outset; by the time a dispute has crystallised, it is too late to implement them.

The Policy Pivot

No private contract can fully insulate a project from sovereign or regulatory intervention. In the scenario above, control over licenses and regulator relationships further concentrates risk.

Renewable projects are especially exposed because their economics depend on long-term tariff, tax incentives, subsidies and licensing frameworks. Governments can change policy. Tariffs can be revised. Tax regimes can shift retroactively. Licences can be amended or delayed.

When that happens, the joint venture structure determines whether the parties can adapt, rebalance risk or exit without disproportionate loss. Robust structures address regulatory exposure from the outset through treaty planning, stabilisation mechanisms and material regulatory event provisions. Valuation assumptions must also reflect the possibility that policy support may not remain static over the life of an asset.

When Fault Lines Compound

As illustrated by the opening scenario, the above structural weaknesses rarely emerge in isolation. Weak control creates opportunities for funding leverage. Funding pressure fuels delay and dispute. That, in turn, leads to deadlock, which undermines the venture’s ability to operate.

Structuring for Stress, Not Harmony

Durable joint ventures are not built around the assumption that relationships will remain harmonious. They are built around the assumption that pressure will eventually arrive. This means operational control that works in practice, immediate funding remedies, exit mechanisms that do not depend on goodwill, real-time transparency and early regulatory risk planning.

Most JV disputes are not surprises. They are structures waiting to fail. The series that follows examines the structuring choices that can stop commercial tension hardening into dispute — not after pressure has arrived, but before it does.