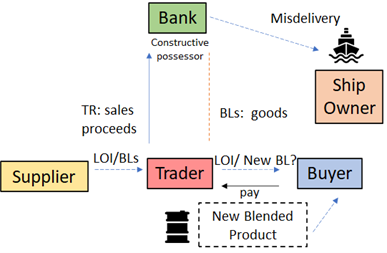

The original bill of lading (BL) is the backbone of trade finance lending arrangements and acts as one of the key security documents should the borrower default: it gives its lawful holder a right to possession of the goods and by extension a potential claim of misdelivery against the shipowner A misdelivery claim is often seen as good security, which can be disposed of by trade finance lenders by way of summary judgment, i.e., without full trial. But to treat the BL as good as gold, the lender must not just hold it as its lawful holder but also do so in good faith – any knowledge that the BL no longer represents the goods might negate the value of the BL in summary enforcement proceedings. In the recent case of The “STI Orchard” (Winson Oil Trading Pte Ltd, intervener) [2022] SGHC 6, the lender, OCBC could not get a summary judgment against the shipowner for its $13 million misdelivery claim, putting into sharp focus the issue of whether the bank could be said to be a holder of the BL in “good faith”.

In a trade finance structure, a BL pledged to the lender as security fulfils the role of a pledge as it gives the lender constructive possession of the goods (i.e., the ability to demand the goods from the shipowner). A trust receipt mechanism is often deployed in trade finance structures alongside the pledge of a BL, so that the borrower can also create a trust over the sale proceeds of the goods in favour of the lender. A lender, overly reliant on the sale proceeds of the goods can inadvertently risk its pledge over the BLs.

Facts

Hin Leong Trading (Pte) Ltd (“Hin Leong”) applied for an LC with OCBC to finance its purchase of oil cargoes. One of the documents required to be presented by Hin Leong’s seller (the “Seller”) for payment under the LC was BLs issued or indorsed to the order of Hin Leong. If BLs were not available, a letter of indemnity issued by the Seller to Hin Leong on the terms set out in the LC could be presented instead. Significantly, OCBC’s LC application form had provided that if a seller was required to present BLs to obtain payment under the LC, the BLs were to be “made out to order of [OCBC]”. At Hin Leong’s request however, OCBC agreed to open the LC on the basis of Hin Leong’s seller presenting BLs issued or indorsed to the order of Hin Leong instead of OCBC.

When the Seller’s bank presented the documents, Hin Leong confirmed acceptance and requested OCBC to grant it a trust receipt loan for the sum due under the LC (the “Trust Receipt Loan”). This would have facilitated the sales proceeds from the Buyer, but critically, of a new blended product – Gasoline 92 RON. In granting the Trust Receipt Loan, OCBC still did not ask for the original BLs. Shortly after granting the Trust Receipt Loan, OCBC learnt of Hin Leong’s precarious financial position and demanded immediate payment of the Trust Receipt Loan. In its capacity as Hin Leong’s agent under the LC terms, OCBC also demanded delivery up of the BLs from the Seller. It received the BLs, which were subsequently endorsed in favour of OCBC. OCBC then commenced proceedings against the Shipowner for misdelivery.

The decision

One of the requirements that a holder of BLs must satisfy when bringing a misdelivery claim is that it became a holder in “good faith”. Previous cases have clarified that good faith in this context simply means honest conduct, and not a broader concept such as observance of reasonable commercial standards of fair dealing. On the facts, the Singapore High Court found that the Shipowner had raised a triable issue as to whether OCBC had become holder of BLs in good faith. The financing arrangements, the Court noted, did not suggest that OCBC was relying on the BLs when it financed Hin Leong’s purchase of the cargo. Rather, OCBC knew that Hin Leong would blend the cargo and sell the new blended product; and it looked to the sale proceeds of the new product as a collateral pursuant to the Trust Receipt Loan. In reaching this conclusion, the Court had regard to the following facts:

- OCBC did not ensure that the BLs were made to its order or indorsed in blank. Rather, it agreed to issue the LC on the basis of the BLs being indorsed to Hin Leong.

- OCBC knew or at least had notice that Hin Leong intended to blend the cargo, and new BLs would have been required for the sale of the new blended product. Yet, it did not ask for the BLs when issuing the Trust Receipt Loan, suggesting that it looked to the sale proceeds as its collateral.

- OCBC only tried to have the BLs endorsed to it after it discovered Hin Leong’s financial difficulties, by which time the blended product had been on-sold pursuant to the Trust Receipt Loan.

In the round, the Court considered that it was arguable that OCBC did not meet the threshold for honest conduct as it did not look to the BLs as security when it financed the cargo, yet was belatedly attempting to bring a claim on the basis of such “security”. The Court was therefore prepared to grant the Shipowner unconditional leave to defend OCBC’s claim for misdelivery.

The Court also found that it was arguable that OCBC had consented to the Shipowner discharging the cargo without the production of the BLs. This is because when OCBC granted the Trust Receipt Loan, it knew or was put on notice that the cargo would be blended by Hin Leong and on-sold as a different product to Hin Leong’s buyer (which would require new BLs). This was unlike previous decisions where Shipowners were found liable to the financing banks for misdelivery, in circumstances where (i) the bank(s)’ customer had pledged the BLs to the bank, and (ii) the BLs were required in the trust-receipt financed on-sale on documents against payment (D/P) terms. In those cases, the bank itself would present the BLs in the on-sale via banking channels, thus retaining custody of the BLs.

Comment

While the Shipowner has been granted unconditional leave to defend OCBC’s claim, it remains to be seen whether the Shipowner will prevail at trial. The Court’s reasoning however is cogent and arrived at by reference to principles from authorities. Regardless of the eventual outcome, the key takeaway from the case is for banks wishing to simplify their recourse against shipowners to obtain possession of BLs indorsed to the bank or in blank rather than over-reliance on the trust recipient mechanism.